Utah Mortgage Guide

Buying Your First Home in Utah

Buying a home for the first time is an exciting yet complex journey, especially when it comes to securing a mortgage, so If you’re a first-time homebuyer in Utah, navigating the various loan options, understanding mortgage rates, and preparing your finances can feel overwhelming. However, with the right guidance, you can confidently make one of the most important financial decisions of your life.

In this guide, we’ll walk you through everything you need to know about getting a mortgage in Utah as a first-time home buyer. We’ll cover different mortgage types, loan programs available in Utah, how to compare interest rates, and mistakes to avoid. By the end, you’ll have a clear strategy to secure the best possible mortgage and move forward with confidence.

What is a Mortgage and How Does It Work?

Mortgage Basics

A mortgage is a loan used to purchase a home because most buyers don’t have the full purchase price in cash, they borrow money from a lender and agree to repay it over time. That is to say that the home itself acts as collateral, meaning if the borrower fails to make payments, the lender can take possession of the property through foreclosure.

Mortgage payments typically consist of four main components:

- Principal – The amount borrowed.

- Interest – The lender’s fee for lending money.

- Property Taxes – Local taxes based on the home’s value.

- Homeowners Insurance – Protection against property damage.

Choosing the right mortgage depends on various factors, including your financial stability, future plans, and current interest rates, so one of the first decisions you’ll make is whether to get a fixed-rate or adjustable-rate mortgage.

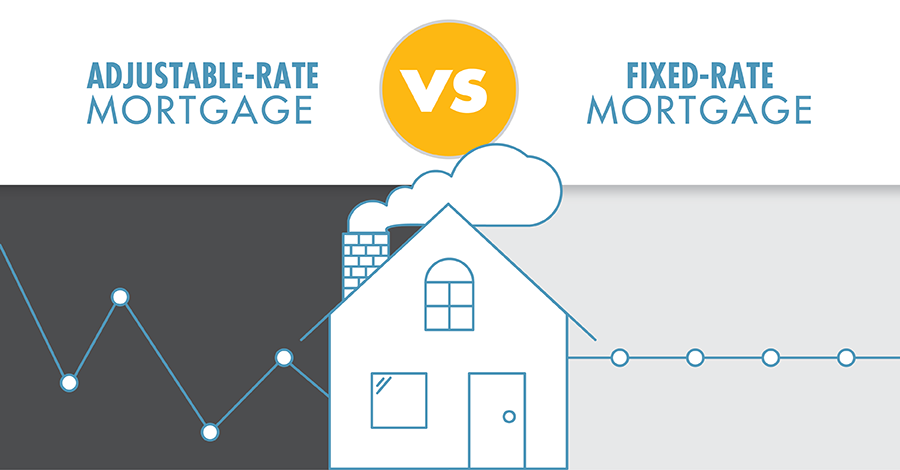

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-Rate Mortgage (FRM)

- The interest rate remains the same throughout the loan term

- Monthly payments are predictable, making budgeting easier.

- Suitable for long-term home ownership.

Adjustable-Rate Mortgage (ARM)

- The interest rate starts lower but adjusts periodically based on market conditions.

- Can be beneficial if you plan to sell your home within a few years.

- Carries higher financial risk if rates increase.

How to Prepare for Buying Your First Home in Utah

Before applying for a mortgage, first-time homebuyers should take several key steps to ensure they qualify for the best loan terms.

Check and Improve Your Credit Score

Your credit score is a critical factor in determining your mortgage interest rate. Lenders use it to assess your financial reliability.

- A FICO score of 740+ qualifies for the lowest interest rates.

- If your score is below 620, your mortgage options may be limited, and your interest rate will be higher.

Check your credit score for free:

If your score is low, focus on paying down debt, avoiding late payments, and maintaining a low credit utilization ratio before applying for a mortgage.

Save for a Down Payment

- In Utah, the average down payment ranges between 5% and 20% of the home’s purchase price.

- A higher down payment often means lower monthly payments and interest rates.

- Some first-time buyer programs allow down payments as low as 3.5% (FHA loans) or 0% (VA and USDA loans).

Get Pre-Approved for a Mortgage

- Mortgage pre-approval helps you understand your budget and strengthens your offer when negotiating with sellers.

- Lenders evaluate your income, debt-to-income ratio (DTI), and credit history before approving a loan.

Great Mortgage Options for First-Time Home buyers in Utah

Utah offers several mortgage programs designed to help first-time homebuyers secure an affordable loan.

Housing Corporation Loan Programs

First Home Loan

- Designed for low-to-moderate income buyers.

- Offers down payment assistance programs.

Score Loan

- Requires a credit score of 620+.

- Allows for higher debt-to-income ratios compared to traditional loans.

Government-Backed Loans

FHA Loan (Federal Housing Administration Loan)

- Minimum 3.5% down payment.

- Requires a credit score of 580+.

VA Loan (For Veterans & Active Military)

- No down payment required.

- No Private Mortgage Insurance (PMI) needed.

USDA Loan (For Rural Areas)

- No down payment required for eligible rural homebuyers.

- Must meet income eligibility guidelines.

These are some options for Utah Mortgage for first home buyers. If you want to know more detail information, you can click here, UHC site. You can find more deep information about programs.

How to Compare Mortgage Interest Rates in Utah

Finding the Great Mortgage Rates

- As of 2024, the average mortgage rate in Utah is around 6.5%.

- Rates fluctuate, so checking multiple lenders and comparison sites is crucial.

- Top Mortgage Rate Comparison Sites:

- Bankrate or NerdWallet

Factors That Impact Mortgage Rates

There are some factors for Mortgage Rates.

Most common factors

Loan Term:

30-year vs. 15-year mortgages—longer terms often have higher interest rates.

APR (Annual Percentage Rate):

Includes interest rate + additional fees.

Lender Type:

Compare local lenders, banks, and credit unions for the best deal

Common Mistakes First-Time Home buyers Should Avoid

- Overextending Your Budget – Buying a home that exceeds your financial capacity can cause stress.

- Ignoring Hidden Costs – Consider property taxes, HOA fees, and maintenance costs.

- Skipping Mortgage Pre-Approval – Without pre-approval, sellers may not take your offer seriously.

Conclusion

Buying a home in Utah as a first-time homebuyer can be an exciting yet complex process, but with the right preparation and knowledge, you can secure the best mortgage for your needs. Understanding the different loan options, improving your credit score, saving for a down payment, and getting pre-approved are all crucial steps to ensure a smooth home-buying experience. Additionally, comparing mortgage rates from multiple lenders and avoiding common mistakes, such as overextending your budget or neglecting hidden costs, can help you make a financially sound decision. By taking the time to research and plan, you can confidently move forward in purchasing your first home in Utah, knowing that you have chosen the best mortgage option available. If you need further assistance, consulting a mortgage expert can provide valuable insights tailored to your financial situation.

If you want to get more tips for Utah Mortgage, you can click here.