Current Mortgage Rates Utah Today – What Homebuyers Need to Know in July 2026

If you’re wondering what current mortgage rates Utah today look like, you’re not alone. As of July 2026, the average Utah mortgage rate 30 year …

If you’re wondering what current mortgage rates Utah today look like, you’re not alone. As of July 2026, the average Utah mortgage rate 30 year …

Buying a first home can feel exciting and overwhelming at the same time. You may be comparing mortgage rates today, trying to understand first time …

In simple terms, dti ratio is the lender’s quick snapshot of how much monthly debt already sits in your budget. If you are getting ready …

Searching for animal shelters near me is often the first step people take when they are thinking about adopting a pet or helping animals in …

Buying a home in Utah is one of the biggest financial decisions most people will ever make, and understanding Utah mortgage rates today is an …

Find help with mortgage rates, home loans and buying a home.

With home prices soaring, mobile homes offer an affordable alternative to apartment living. Learn how to get pre-approved for a mobile home loan in Utah today!

If you’re wondering what current mortgage rates Utah today look like, you’re not alone. As of July 2026, the average Utah mortgage rate 30 year …

Buying a first home can feel exciting and overwhelming at the same time. You may be comparing mortgage rates today, trying to understand first time …

In simple terms, dti ratio is the lender’s quick snapshot of how much monthly debt already sits in your budget. If you are getting ready …

Searching for animal shelters near me is often the first step people take when they are thinking about adopting a pet or helping animals in …

Buying a home in Utah is one of the biggest financial decisions most people will ever make, and understanding Utah mortgage rates today is an …

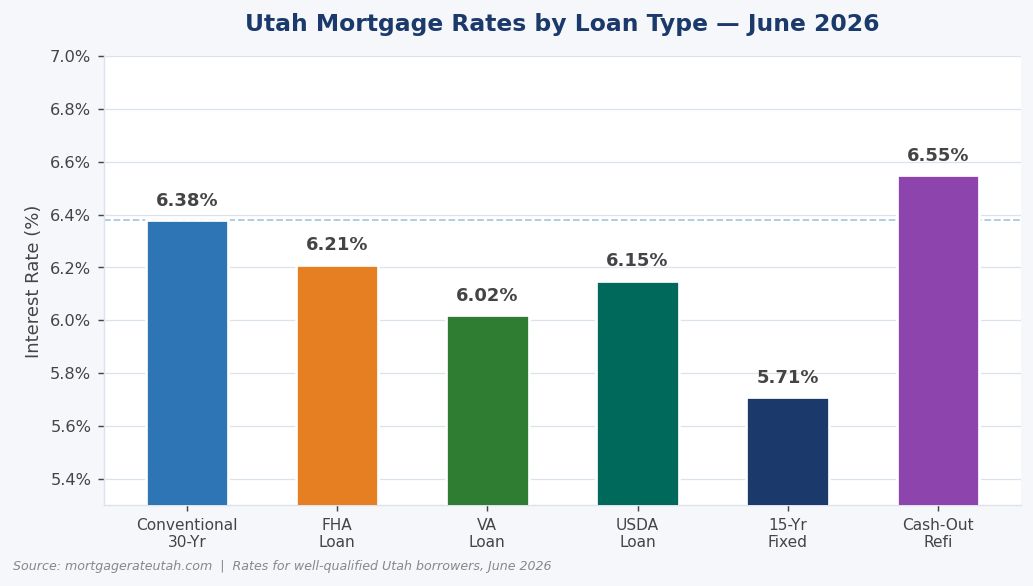

If you’re planning to buy a home this year, finding the best mortgage rates in Utah 2026 can make a significant difference in your monthly …

Utah’s housing market has cooled slightly from its pandemic-era peak — but for first-time buyers, the challenge of affording a home has not gone away. …

Mortgage Calculator ALT image tag: mortgage preapproval, house with coins Utah Mortgage rates 2026 are shifting quickly, and buyers need to understand what’s driving these …

Shopping for a home in Utah? Or wondering whether now is the right time to refinance? Understanding current mortgage rates is the single most important …

contact@alpacapers.com

Phone: +1 234 567 8900

Fax: +1 234 567 8900

contact@alpacapers.com

Phone: +1 234 567 8900

Fax: +1 234 567 8900